AsiaTechDaily – Asia's Leading Tech and Startup Media Platform

The Infrastructure Paradox: Financing Hardware-Heavy Climate Tech Without Bloating Venture Capital Balance Sheets

Why clean-tech scale demands a structural split between high-cost venture equity and institutional debt engineering.

The global venture capital ecosystem is facing a critical bottleneck in its pursuit of decarbonization. While institutional investors eagerly chase the rapid scaling curves and high gross margins of software-driven climate solutions, the physical reality of hitting carbon neutrality requires massive deployments of hardware. Real-world mitigation relies on the construction of physical infrastructure: business-to-business (B2B) charging grids, localized battery manufacturing hubs, long-life recycling facilities, and extensive commercial vehicle fleets.

This necessity creates a fundamental paradox. Funding heavy, long-gestation hardware assets using pure, high-cost venture capital equity destroys startup capital efficiency. It bloats cap tables, dilutes founders prematurely, and forces mismatched growth expectations onto traditional venture fund timelines. As the climate-tech sector shifts from early-stage technology validation into widespread execution, the industry is undergoing a structural realignment. Scale is no longer just a technological milestone; it has become an exercise in advanced capital engineering.

The primary focus of consumer-facing capital allocation has historically gravitated toward electric vehicle (EV) original equipment manufacturers (OEMs) and high-visibility battery branding. However, this asymmetric focus has left the operational backbone of the ecosystem severely exposed. Essential layers of the value chain, such as heavy component manufacturing, B2B charging grids, and end-of-life battery recycling, routinely struggle to secure traditional venture backing.

These hidden, infrastructure-heavy layers are critical to building a resilient, circular ecosystem. Yet, they are frequently overlooked by institutional investors due to their longer development cycles and complex, multi-tiered operational models. While conversing with AsiaTechDaily regarding these market inefficiencies, Vasudha Madhavan, Founder and CEO of Ostara Advisors, highlighted that investor attention remains fundamentally misaligned across the clean mobility landscape.

“While EV OEMs and battery tech get most of the attention, critical areas like component manufacturing, B2B charging infrastructure, battery recycling, and supply chain tech are still underfunded,” Madhavan observed. “These segments are essential to building a resilient ecosystem but often get overlooked due to longer gestation cycles and complex models.”

To unlock these capital-intensive bottlenecks, a broader investment perspective is required. This shift includes tapping into alternative, international capital pools accustomed to underwriting asset-heavy infrastructure bets, alongside correcting persistent blind spots around leadership diversity. In a heavily technical and male-dominated space, widening the executive and evaluation lens is increasingly recognized as a core risk-mitigation strategy that drives more balanced capital allocation decisions.

Capital Architecture: Blending DFIs and Venture Equity

To bypass the capex trap without choking growth, forward-thinking climate-tech companies are designing distinct, bifurcated capital structures. Rather than absorbing expensive equity dilution to buy heavy machinery or real estate, startups are isolating their technology risk from their deployment risk. Under this framework, high-cost venture equity is reserved strictly for software development, IP creation, and organizational scaling, while patient institutional debt is utilized to fund physical assets.

A crucial driver of this new financial playbook is the strategic deployment of low-cost debt sourced from Development Financing Institutions (DFIs) and specialized, energy-transition-focused financing vehicles. These institutions provide the long-term, low-interest capital required to absorb the slow return on investment (ROI) typical of infrastructure deployments, particularly as hardware expands into fragmented secondary and tertiary markets.

Speaking with AsiaTechDaily, Madhavan mapped out exactly how contemporary infrastructure startups are engineering their balance sheets to preserve equity while fueling aggressive asset expansion.

“Most companies in these space do end up raising a mix of debt and equity to fund their growth ambitions,” Madhavan stated. “Low-cost debt from Development Financing Institutions (DFIs) or Energy Transition-focused financing institutions can go a long way in supplementing high-cost equity when investing in critical infrastructure or assets required to grow these businesses.”

This complementary relationship creates a virtuous cycle. Policy clarity and international climate commitments de-risk the sector, allowing DFIs to provide baseline asset financing. This institutional debt cushion then protects the startup’s cap table, making the company far more attractive to traditional private equity and venture capital funds looking for clean, non-bloated balance sheets.

Real-World Blueprints for Asset-Light Execution

This structural shift in capital allocation is already visible across the regional transport and logistics landscape. Prominent players are actively demonstrating that massive physical scale can coexist with lean corporate cap tables through tactical business modeling and diversified funding rounds.

- The Corporate Commute Model: Corporate Transport-as-a-Service (TaaS) platform Routematic successfully raised a $40 million Series C funding round led by the Fullerton Carbon Action Fund and Shift4Good. By utilizing an asset-light framework focused on driver contracting and AI-powered dynamic routing, the company has managed to aggressively expand its operational footprint across dozens of cities while targets include converting a significant portion of its corporate commute fleet to electric vehicles.

- The Fleet Financing Hybrid: Last-mile EV rental and logistics platform Zypp Electric has consistently paired its venture equity rounds with structured debt facilities from institutional lenders like Northern Arc Capital and Anicut Capital. This dual strategy allows the platform to deploy tens of thousands of new electric two-wheelers into commercial delivery networks without relying exclusively on high-cost venture capital to purchase physical vehicles.

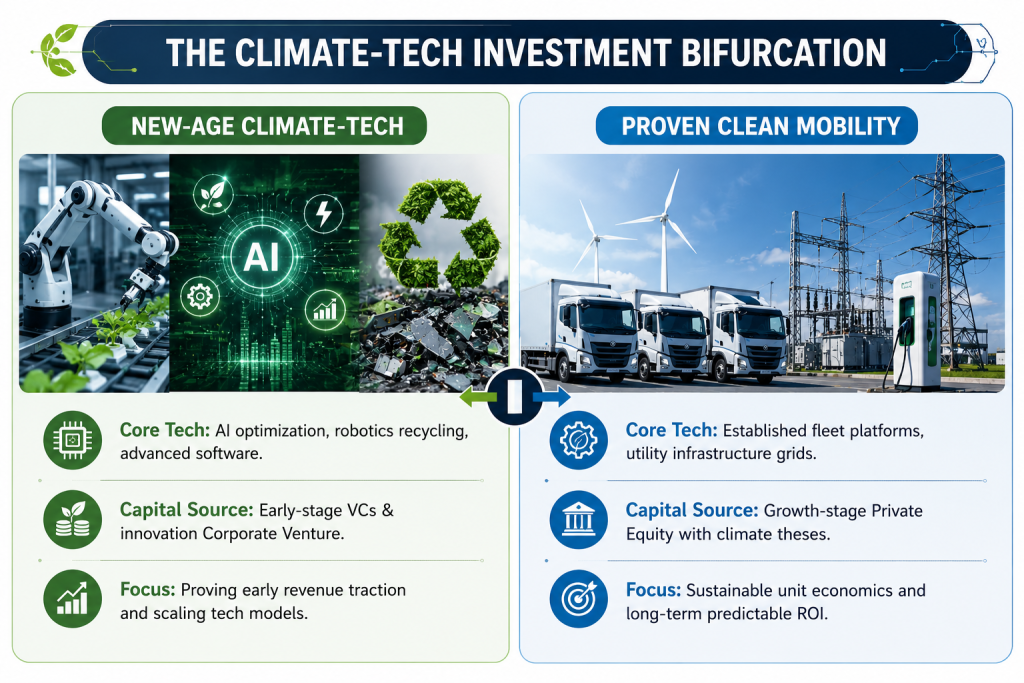

These operational blueprints reflect a broader bifurcation in how institutional investors evaluate emerging clean tech. The diligence process has effectively divided into two distinct tracks based on asset profile and technological maturity.

The Unit Economics Ultimatum

As macroeconomic conditions place greater scrutiny on runway and paths to profitability, the era of unmitigated capex expansion backed by venture equity is over. In a tightening fundraising environment, the mandate for climate-tech founders has shifted from pure market-share acquisition to defensive, structural sustainability.

Long-term viability requires builders to maintain strict geographic and customer-segment de-risking. Government policy will continue to set the baseline direction via regulatory incentives and net-zero targets, but private capital will dictate the efficiency and speed of execution.

Ultimately, the future of the clean energy transition belongs to founders who view capital structure as an architectural science. By keeping growth momentum anchored to robust unit economics and leaving the capital-intensive infrastructure heavy lifting to specialized institutional debt, early movers will secure the scale needed to win the market without breaking their balance sheets. This ongoing research index tracks global asset finance, equity trends, and capital allocation across clean energy sectors, providing direct macroeconomic verification of the shifting balance between venture capital and institutional debt structures worldwide.

⚡ Quick Takeaways

- The Venture Capital Paradox: Traditional high-cost venture equity is poorly suited for funding long-gestation, physical climate hardware, as it bloats cap tables, dilutes founders, and forces unnatural growth timelines on asset-heavy operations.

- The Back-End Underfunding Gap: While consumer-facing EV OEMs and battery brands capture mainstream headlines, critical foundational layers—such as heavy component manufacturing, B2B charging grids, and circular economy recycling tech—remain severely underfunded.

- Advanced Capital Engineering: Leading climate-tech startups are decoupling their technology risk from their deployment risk, reserving venture capital for software and IP creation, while utilizing low-cost debt from Development Financing Institutions (DFIs) to fund physical assets.

- Bifurcated Due Diligence: The investment landscape has split into two tracks: early-stage VCs and corporate venture capital backing high-innovation software/robotics, and growth-stage private equity backing proven infrastructure models with predictable unit economics.

- The Resilience Mandate: Long-term market survival demands an unyielding focus on robust unit economics and structural, geographic de-risking over pure growth hype and policy reliance.

Similar Articles