AsiaTechDaily – Asia's Leading Tech and Startup Media Platform

Why Singapore Became the World’s Wi-Fi 7 Leader — and Why Few Others Can Follow Yet

A new Ookla report shows Asia-Pacific’s wireless networks splitting into two distinct tiers, with regulatory timing and telco strategy — not consumer demand — emerging as the deciding factor in who gets to next-generation Wi-Fi first.

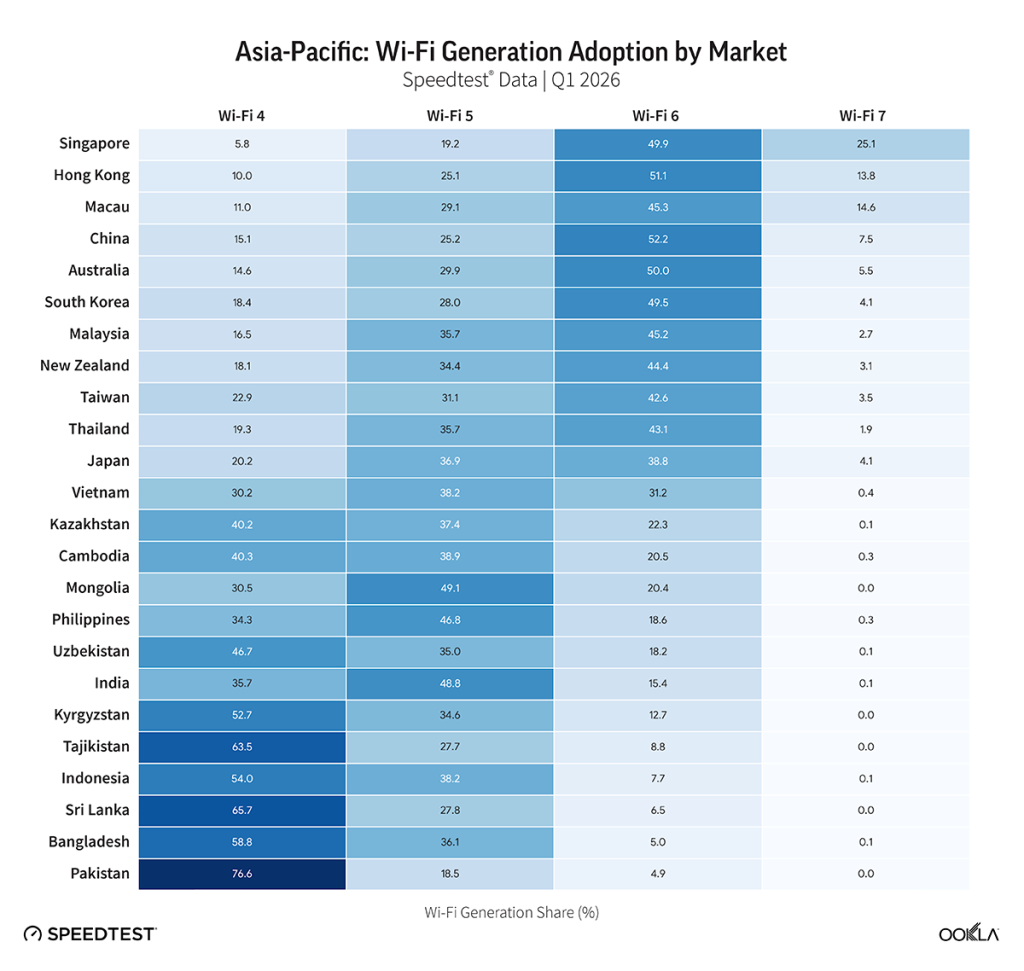

Asia-Pacific’s Wi-Fi networks are moving in two directions at once. According to a new report from network intelligence company Ookla, based on Speedtest data from the first quarter of 2022 through the first quarter of 2026, the region’s fastest-growing standard, Wi-Fi 6, has expanded fivefold over four years, from 4.0% to 20.6% of samples. Yet Wi-Fi 4 — a standard now well over a decade old — still accounts for 40.4% of all APAC connections, with Wi-Fi 5 holding nearly as large a share.

The picture that emerges isn’t simply “APAC is behind.” It’s a region splitting into two tiers: a small group of markets, led by Singapore, that have already leapt to Wi-Fi 7 and the 6 GHz spectrum that powers it, and a much larger group still running on hardware from the early 2010s. What separates the two, according to Ookla’s analysis, has less to do with what consumers want and more to do with regulatory timing and how aggressively telcos choose to push upgrades.

The Singapore Anomaly

Singapore doesn’t just lead Asia-Pacific in next-generation Wi-Fi — it leads the world. As of Q1 2026, 25.1% of Singapore’s Wi-Fi samples were running on Wi-Fi 7, the highest share of any country Ookla tracks. The country also recorded 13.3% of its Wi-Fi traffic on the 6 GHz band, far ahead of the next-best APAC performers: Hong Kong (5.0%), Japan (4.2%), and Australia (3.6%). For context, the region as a whole sits at just 0.5% 6 GHz usage.

Ookla’s data suggests this wasn’t an organic consumer-driven shift. Singapore’s government pushed providers to roll out 10 Gbps home broadband, and crucially, made the case to consumers that their existing Wi-Fi 6 or 6E routers simply couldn’t deliver those speeds — only Wi-Fi 7’s wider 320 MHz channels and multi-link operation could. Telcos followed by bundling Wi-Fi 7 hardware directly into multi-gigabit subscriptions rather than leaving the upgrade decision to individual households.

The effect shows up clearly at the operator level: according to Ookla, 27% of Speedtest users on Singaporean telco MyRepublic are already connecting via Wi-Fi 7, followed by ViewQuest (22%), StarHub and Singtel (21% each), and M1 (20%).

Speaking to AsiaTechDaily, Affandy Johan, an industry analyst at Ookla, said the lesson for other markets is specific rather than universal. “Singapore serves as a powerful blueprint, achieving a world-leading 25.1% Wi-Fi 7 adoption rate. This success was not organic. It was catalyzed by aggressive government initiatives pushing 10 Gbps home broadband speeds,” he said. “Crucially, local telcos did not leave hardware upgrades to the retail market. They proactively bundled Wi-Fi 7 customer premises equipment into their multi-gigabit subscriptions.”

But replicating that requires a fairly narrow set of conditions. “For other markets to replicate this, they require a mature ecosystem—widespread fiber-to-the-home penetration, consumers willing to pay for multi-gigabit tiers, and highly coordinated ISP efforts to deploy capable Wi-Fi 7 hardware,” Johan said.

It’s the Spectrum, Not the Phones

The report’s most counterintuitive finding may be this: consumer devices are not the bottleneck. Globally, 61.4% of Android Speedtest samples in Q1 2026 came from phones already capable of Wi-Fi 6 or newer. Most people, in other words, are carrying hardware that’s ready for an upgrade their home network can’t yet deliver.

The constraint, instead, sits with regulators and infrastructure. Much of APAC has been slow to open the 6 GHz band — the spectrum that gives Wi-Fi 6E and Wi-Fi 7 their performance headroom — for unlicensed Wi-Fi use. South Korea is one of the few APAC markets, alongside Kazakhstan, to have followed the U.S. in allocating the full 6 GHz band for unlicensed use. China has taken the opposite path entirely, reserving the whole band for mobile (IMT) services with an eye toward 6G — a decision that has pushed Chinese device makers toward dual-band Wi-Fi 7 routers that skip 6 GHz altogether to keep costs down. That dynamic helps explain why 7.5% of Wi-Fi samples in China are already on Wi-Fi 7 — the highest share in APAC — despite the country having essentially no 6 GHz Wi-Fi traffic. Japan and South Korea each sit at 4.1% Wi-Fi 7 share, broadly in line with their fiber infrastructure and telecom competition.

India offers a useful illustration of how much regulatory timing matters: the government spent years deliberating whether to assign the 6 GHz band to mobile operators or Wi-Fi, only formally allocating the lower 6 GHz band for Wi-Fi use in January 2026 — a decision that puts India several years behind markets that moved in 2020.

Johan framed the region’s reliance on older standards as a structural issue rather than a preference. “The reliance on older standards across the Asia-Pacific region is dictated by home infrastructure constraints, not consumer demand,” he told AsiaTechDaily. Comparing the region to North America — where Wi-Fi 6 already commands 57.5% of samples, and 6 GHz usage grew sixfold in two years to 13.8% — he pointed to two factors: “The U.S. and Canada opened the full 1,200 MHz of 6 GHz spectrum early, and local internet service providers actively bundled capable routers into broadband plans, accelerating consumer adoption. Conversely, most of the APAC market only opened the lower 6 GHz band. Sluggish regulatory approvals weaken the commercial case for hardware upgrades.”

A New Complication: AI Is Making Routers More Expensive

One factor the report flags as an emerging headwind has nothing to do with spectrum policy at all. The same AI infrastructure boom driving demand for high-performance memory and processing chips in data centers is also pushing up component costs across the broader semiconductor supply chain — costs that flow directly into the bill of materials for both smartphones and home routers.

For internet service providers already weighing the economics of bundling next-generation hardware, that’s an unwelcome variable. Higher CPE costs make the business case for subsidizing Wi-Fi 7 routers — the strategy that worked in Singapore and North America — harder to justify, and could push some providers toward cheaper, less capable equipment instead. It’s a reminder that the AI boom’s effects on connectivity infrastructure aren’t limited to data centers; they’re starting to show up in the cost of the router sitting in someone’s living room.

What Comes Next

Globally, Wi-Fi 7 remains nascent at just 1.8% of samples, though Omdia forecasts it will grow at a 35.2% compound annual rate to reach 13.8% of the installed base by 2030 — by which point Wi-Fi 6 is expected to still dominate with a 62.0% share. Wi-Fi 8, the next standard after that, is expected to begin appearing around 2028, with a different value proposition entirely: rather than chasing peak speeds, it’s being designed for reliability, lower latency, and more consistent performance in crowded environments like multi-device households and dense apartment buildings.

Johan argued this should shape how operators think about current investment cycles. “Operators and manufacturers should treat Wi-Fi 7 as the foundation for the multi-gigabit era, building on its 320 MHz channels and multi-link operation,” he said. “Wi-Fi 8 is expected by 2028, but it focuses its gains less on headline speed and more on reliability, lower latency, and better roaming in dense environments. The practical course is to keep investing in Wi-Fi 7 now, and in 6 GHz radios where the spectrum is available, since that hardware and spectrum experience carries straight into Wi-Fi 8.”

For most of Asia-Pacific, that “practical course” still depends on a step that hasn’t happened yet in many markets: regulators deciding how much of the 6 GHz band Wi-Fi actually gets to use. Until that’s resolved, the gap between Singapore’s living rooms and the rest of the region’s is unlikely to close on its own.

Quick Takeaways

- Wi-Fi 6 adoption in Asia-Pacific grew five-fold from 4.0% in Q1 2022 to 20.6% in Q1 2026, according to Ookla.

- Despite rapid growth in newer standards, Wi-Fi 4 still accounts for 40.4% of APAC usage, highlighting the region’s uneven infrastructure upgrade cycle.

- Singapore leads the world in Wi-Fi 7 adoption at 25.1%, driven by strong fiber infrastructure, government-backed broadband initiatives and aggressive telecom bundling.

- South Korea and Japan each recorded 4.1% Wi-Fi 7 adoption, while China reached 7.5%, partly due to lower-cost dual-band Wi-Fi 7 routers.

- While conversing with AsiaTechDaily, Ookla said infrastructure constraints, fragmented 6 GHz spectrum policy and slower ISP upgrade cycles remain the biggest barriers to adoption across APAC, rather than consumer device limitations.

Similar Articles